In an article that I posted on 2 November 2015 titled, “Europe is at a crossroad: let’s identify the problems”, I presented an opinion that severe problems exist in the EU/Eurozone.

After the 2008 Global Financial Crisis, more and more “economic experts” have realised that there are some severe short-comings in the “monetary system architecture” that is embodied in the neo-classical economic model that most first world, western countries follow. And if it wasn’t enough that the hidden faults in the EMU came to the fore as the European Debt Crisis spiked in late 2012, like a slap in the face, the EMU received a kick in the nuts as the deficiencies in the monetary system model added further fuel to the fire.

My starting point was the article written by Pavlos Papageorgiou in 2012. The most troubling thing is that, from that date until the present, no real improvement in the situation can be noted. In fact, it has got worse!

And it is not just me that has come to this conclusion.

Peter Praet, who is an ECB Executive Board Member and the ECB Chief Economist, gave a presentation at the BVI Asset Management conference in Germany on 1 October 2015, showing one devastating chart after another on how the euro has failed the Eurozone economy. The underlying theme was hardly one of the celebration of a success story and optimism for the future. Quite the contrary!

Perhaps Praet was dong a little “whistleblowing” on the real state of affairs in the Eurozone.

Subsequently, Don Quijones (Raging Bull-Shit & Wolf-Street), wrote an excellent follow up article that makes all of the technical graphs understandable to the person-in-the-street.

“Euro Sinks Deeper into Limbo

by Don Quijones (1 November 2015)

Things are not looking good for the euro. Out of its 16 years of existence, the euro has spent seven years in crisis. Rather than serving as the EU’s springboard to global dominance, as had been planned, the euro could well be its ultimate undoing.

The European single currency’s share of global transactions has dramatically shrunk in the last two years, from 40% in January, 2013, to 27% today. Europe’s share of global earnings has halved from just over 40% in 2009 to just over 20% today. It’s hardly what you’d call a success story.

There seems to be no agreement among Europe’s major power brokers about how to put the project back on track. If recent statements out of London, Frankfurt, Paris and Berlin are any indication, there is a growing resignation that Europe’s unification may have reached its outer limits. At least for now.

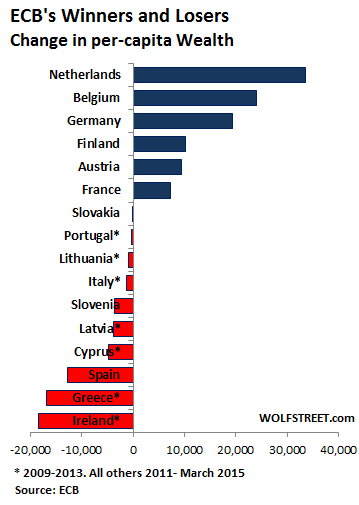

Winners and Losers

The first murmurings of disquiet came from the Frankfurt-based ECB, which just released some data on the biggest winners and biggest losers of the debt crisis and the ECB’s monetary policies, such as its negative deposit rates, QE, and all the other schemes it has used over the years to create that special wealth effect that would get the Eurozone economy moving.

The results are hardly a surprise: the biggest losers are Ireland, Greece and Spain and the biggest winners the Netherlands, Belgium, and Germany.

Between 2009 and 2013, Ireland lost more than €18,000 per capita while Spain saw its average wealth shrink by €13,000 per person – as a result not only of their respective rescue programs but also the burst of their spectacular real estate bubbles. The Greeks, meanwhile, saw their national wealth contract by €17,000 per capita.

By contrast, in the Netherlands, Belgium, and Germany, wealth grew during the same period by €33,000, €24,000, and €19,000 per capita respectively, due in large part to the massive influx of the ECB’s flood of liquidity and of financial investments, mainly from the euro’s loser nations.

As its monetary policies spread over the Eurozone, the ECB is powerless to reduce these gaping disparities that its own policies helped create, it said. Its economic stimulus plan, if you can call it that, distributed funds among Eurozone nations based purely on their relative size, without taking into account the particular economic needs of each one.

As its monetary policies spread over the Eurozone, the ECB is powerless to reduce these gaping disparities that its own policies helped create, it said. Its economic stimulus plan, if you can call it that, distributed funds among Eurozone nations based purely on their relative size, without taking into account the particular economic needs of each one.

The Limits of Unity

To correct the imbalances between stronger and weaker economies, a centrally coordinated system of financial transfers is needed that allows money to flow from the currency bloc’s richer nations to poorer ones. That’s the report’s convenient conclusion.

It’s the same old tired dream of full-blown fiscal union, or what Germans deride a “transfer union,” which Germany continues to oppose, especially given the seeming reluctance of many of the Eurozone’s “loser” nations to embrace a never-ending cycle of labor reforms, shrinking wages, and internal devaluations.

Even amongst Europe’s ranks of senior technocrats, doubts are beginning to emerge.

“Fiscal union is not a panacea,” Olivier Blanchard, the former chief economist of the IMF, told The Telegraph. “It should be done, but we should not think that once it is done, the euro will work perfectly, and things will be forever fine.”

Quite the contrary: Any mechanism to transfer funds from strong to weak nations – which has been fiercely resisted by Germany – would merely mask the fundamental competitiveness problems that will always plague struggling member states, he said.

Without the power to devalue their currencies, peripheral economies would forever be doomed to endure “tough adjustment” such as slashing their wages, to keep up with stronger member states, Blanchard said. This is exactly what has happened in Spain, which many economists and eurocrats have hailed as a poster child for Brussels’ austerity diktats. Mr Blanchard, like myself, is not buying the hype:

When people talk about the Spanish miracle, I react. When you have 23% unemployment and 3% growth, I don’t call this a miracle yet.

Back in Limbo

A few months ago Emmanuel Macron, France’s Minister of the Economy, and Sigmar Gabriel, the German Vice-Chancellor, unveiled an audacious master plan to achieve greater fiscal and social harmonization in the Eurozone.

“A new, staged process of convergence is needed,” the authors wrote. This would involve not only structural reforms (labor, business and the environment) and institutional reforms (functioning of economic governance) but also social and tax convergence – all in the name of addressing the “critical flaws in the architecture of monetary union.”

Now, just a few months later, the plan has already been shelved. With Germany once again digging in its heels, the chances of Europe agreeing on a fiscal pact – even a significantly diluted one – appear to be fading. Even the banking union – completed last year to great public fanfare, including pitched street battles and burning vehicles – remains half-baked, much to the ire of Western central bankers.

At last week’s EU Summit, Berlin made clear it would veto any proposals for a joint insurance of bank deposits, without which the banking union is destined to remain an empty shell. According to the FT’s Walter Machau, the German position is unrelenting, with the result that the Eurozone is once again back in limbo:

It is time to grow used to the thought that neither the Eurozone crisis, nor any other crisis for that matter, will bring about lasting institutional change. For sure, it brings about reports like the one written by the presidents of five EU institutions. They contain a few worthy discussion points. But the original design of a monetary union without a joint fiscal capacity is going to persist. The Eurozone is, and will remain, a modern gold-standard type, fixed-exchange rate system.

This effectively means the deep-seated imbalances that have consigned countries like Ireland, Greece and Spain to the scrap heap of economic development while boosting the competitiveness of Europe’s richest economies are here to stay for the foreseeable future.

The good news? Given that the main alternative – besides scrapping the euro project altogether – is granting an unprecedented amount of power over the lives of half a billion people to institutions that have virtually zero democratic legitimacy and accountability and that have done nothing to earn the public’s trust, perhaps muddling along is the least bad, really bad option on offer.”

What was the saying again? There are lies, dammed lies and above all, statistics.

This one proves that Dutch wealth grew (from 2009 to 2013) by € 33.000,- per capita. I wonder how.

For the first time in 4 years civil servants got a pay rise, partly payed out of lower pension contributions (=lower pensions at the age of retirement).

Massive cuts in social programs for the elderly and child benefits. In 2015 1/3 of the houses are still “under water”. That is, the value of a the house is still below its mortgage.

And guess what, despite all this our wealth has increased to the tune of an average annual income

LikeLike

Maybe there is a select group of people (bankers? politicians?) who are really coining it at the average person’s expense?

Maybe there are some rich, Dutch oligarchs that no one knows about?

If that is not the case, then may I suggest that you challenge these facts with the source of the statistics, the ECB.

PS. At the risk of really upsetting you, I would add that you are starting to sound like Yanis V. when he was in the Eurogroup meetings at the height of the Greek crisis, earlier this year.

LikeLike

The point I’m trying to make is that these statistics say very little about the situation on the ground.

Take for example Greece GDP. Everybody seems to agree that this only represent 70 % of the total GDP and 30% of national income isn’t declared. Implementing a better tax regime (more or less comparable with northern Europe) would result in a massive increase in GDP.

Another study reveals that the Greek professional class only declares (and only pay taxes over) half their income.

Italy’s sovereign debt is almost double Dutch sovereign debt, but private debt is much lower than in Holland. If you take both together there isn’t much difference. So what should be the solution?

The Dutch lowering their taxes and increase their sovereign debt, so they can pay of their private debt (like mortgages) or the Italians raise their taxes to lower their sovereign debt. (what almost certainly will result in a increase in private debt).

Me contradicting Yanis? As a finance minister sure. As an economist hardly. Based on his analysis my conclusion was, in the long run Greece would have been better off if they had left the Euro. In an orderly fashion. Like Stauble proposed.

Why stick to a currency union that breaks up in the near future anyway.

So don’t worry about upsetting me 😉

LikeLike

Pim,

Point taken.

Surprisingly, you have alluded to something that I have concluded is the real, underlying “cause” of the Eurozone crisis.

This is the subject of an upcoming post.

LikeLike